What exactly is your AI moat?

July 2, 2026 · James Wang

Every founder building on top of the frontier models eventually runs into the same question, and most of them can’t answer it.

I met one recently who couldn’t. He had a strong technical team, lived the problem himself, had design partners already lined up. I wouldn’t call what he was building a ChatGPT wrapper… his product used agents in a creative way and solved a real workflow problem for his users. But it also wasn’t anything that couldn’t be replicated by someone with enough motivation.

I still couldn’t get to yes, and the reason is that question. What happens when the company that makes the model decides to build this themselves?

He had an answer, technically. His team was better, faster, and closer to the customer. Every word of that was true, and none of it was a moat.

The Word Founders Hide Behind

I’ve written before about the model layer commoditizing and the labs walking down the stack into deployment, so I won’t relitigate it. You can find that piece here. Take it as settled that the platform is coming for the application layer… the platform already told us so, twice, with about five and a half billion dollars behind it.

What I want to focus on is a different mistake, because it’s the one that traps good founders. The word is “infrastructure,” and it’s doing a lot of dishonest work in pitches right now.

Here’s the problem with the word. Infrastructure describes where you sit in the stack… a technical middle layer between the model and the customer’s data or workflows. It says nothing about whether you can hold that position. But the word borrows its gravity from the physical kind. Roads and power grids feel permanent because nobody builds a second bridge next to yours. Software extends no such courtesy. The platform can build the second bridge in a quarter, toll-free, and its marginal cost of doing so keeps falling.

So when a founder says infrastructure, everything they mean by it can be true. The orchestration is complex, the pipeline took real engineering, the team is excellent. And none of it answers the question the word is pretending to answer, because hard to build and hard to take are different properties. Position is not defensibility. Switching costs can be part of the answer, but only when they outweigh the value of the platform’s offer, and that math rarely works when the platform gives the model away.

The Test

So here’s the test I’d hand any founder building in AI, and it’s the one I was thinking aboutwhile he talked.

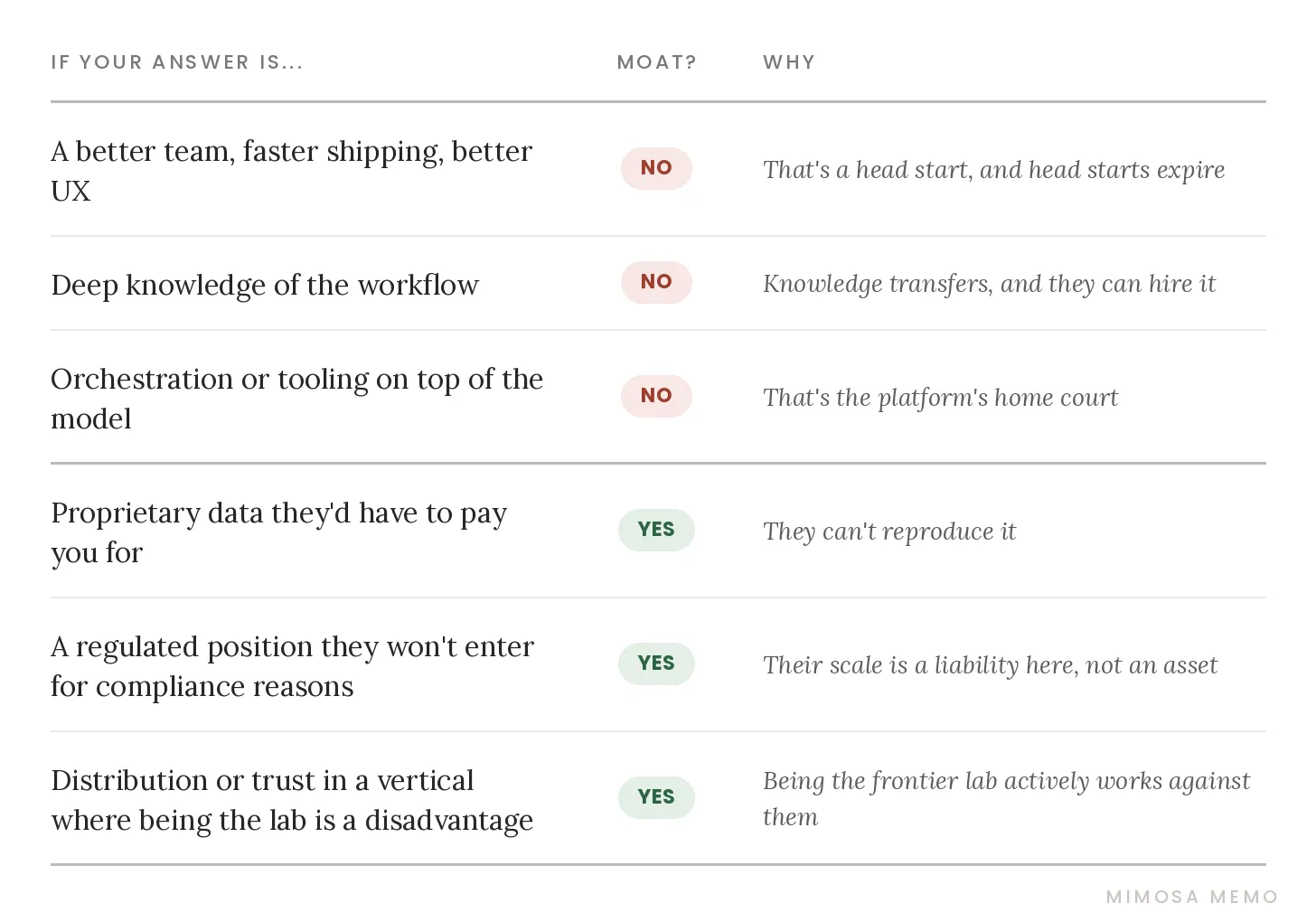

Assume the frontier lab wakes up tomorrow, looks at your exact market, and decides to build your exact product. They have the model, the compute, the distribution, and cheaper access to all three than you’ll ever have. What do you own that they can’t reproduce just by deciding to?

Everything on the top half can be reproduced with a decision and a quarter of engineering time. Everything on the bottom half would cost them years, or capital they’d rather point at you, or a market their own scale disqualifies them from. You can build genuine infrastructure out of nothing but top-half assets, and plenty of founders have. The bottom half is what makes it durable. Something the platform finds hard to reproduce, rather than something you found hard to build.

The Problem With My Own Test

Run that test on any seed-stage company and it fails. Proprietary data, regulatory positions, owned distribution… these are assets that accrete with scale and time. They are, almost by definition, late-stage assets. A founder with a working product and a handful of design partners doesn’t have them yet, and can’t. So at the stage I actually invest, the test is structurally guaranteed to return “nothing.” Applied literally, it isn’t a filter. It’s a reason to never write an application-layer check.

Cursor is the case that bucks the trend, and as of two weeks ago, it’s also the case that finishes the argument. Go back two years and run the test on them. Every answer lives on the top half of my table. Better team, faster shipping, better product, all of it built directly on someone else’s models. The labs did exactly what the framework predicts… they walked down the stack and shipped their own coding agents straight onto Cursor’s turf. And for a while, Cursor kept winning anyway, which made them everyone’s favorite rebuttal to everything I just wrote.

Then the framework caught up. Over the past year, Cursor’s share of the AI coding market roughly halved while Anthropic took half the category for itself. And underneath the share numbers sat an uglier structural problem… Cursor’s cost of goods was the platform’s revenue. Every token they served made their competitor stronger. Two weeks ago the story resolved the only way it could have resolved well. SpaceX bought them for sixty billion dollars in stock.

Cursor owned the daily workflow of the exact developers who decide which AI tools become standard, plus enterprise relationships across most of the Fortune 500. The one lab that had gone nowhere in coding looked at that position and decided sixty billion in stock was cheaper than continuing to fail at reproducing it. “They can’t reproduce it by deciding to” turns out to have a price, and now we know roughly what it is. But the top half was real too. The head start expired on schedule. Cursor never actually beat the platforms. It got squeezed by them and then sold to one, about a year after turning down OpenAI twice.

Which is the lesson I take from it. The head start was never the moat. It was the budget for one, and Cursor spent theirs about as well as a head start can be spent… they converted speed into workflow ownership and enterprise trust fast enough that when the squeeze arrived, they were selling an asset instead of running out of one.

That reframes the question for the stage I invest at. Asking a seed founder “what’s your moat” is asking in the wrong tense, because the answer is nothing and we both know it. The real question is what you’re converting the head start into, and how long you think you have. A founder who says “our team is better” as the final answer fails. A founder who says “our team is better, which buys us maybe eighteen months to lock up data nobody else can assemble” passes. Same facts. Entirely different company.

And that’s also why “we’re too small for them to care” doesn’t help you. It might even be true for a while, but indifference has a shelf life… it tells you how long the conversion window stays open, and the window runs on the platform’s schedule, not yours. Ask Cursor, who went from category darling to seller in about a year. If the countdown runs that fast for the best-executed application company of the cycle, it runs faster for everyone else. The solution was never to orchestrate the models better than anyone. That’s competing on the platform’s court with the platform’s ball. The fix is to spend the window acquiring the bottom half of that table… lock up data nobody else can assemble, build distribution you own instead of rent, and do it before the clock runs out.

When There’s No Bottom Half

There’s one more answer I should have been willing to say out loud in that meeting, because it’s the most useful thing anyone could have told him.

Some products have no bottom-half square available at any stage. No data worth locking up, no regulatory shelter, no vertical where being the lab is a disadvantage. If you map your product against that table and every path leads to the top half, you’re not building a company. You’re building a feature. That is not an insult… features get acquired all the time, and the move is to run that process while the platform still wants to buy what it hasn’t built, not after it ships your version as a free update.

And before you object that “sell to the platform” sounds like a consolation prize, look at what just happened. Cursor’s exit was that exact play, executed with maximum leverage… multiple bidders, category leadership, and a buyer who needed them more than they needed the buyer. The sale path isn’t the failure mode. It’s a strategy with an enormous range of outcomes, and what determines where you land in that range is the same bottom half of the same table. SpaceX didn’t pay sixty billion for a head start. It paid for what the head start had been converted into. The founder with no bottom half sells without leverage, on the platform’s timeline, at the platform’s price.

I hope the founder I met goes and does the conversion. The team is good enough for it… but the team was never the question. At seed, everyone’s answers live on the top half of that table, Cursor’s included. The difference between a pass and a check was never whether he had a moat. It was whether he could tell me what the head start was for.