Dallas Cracked the Top 10. Now What?

May 19, 2026 · James Wang

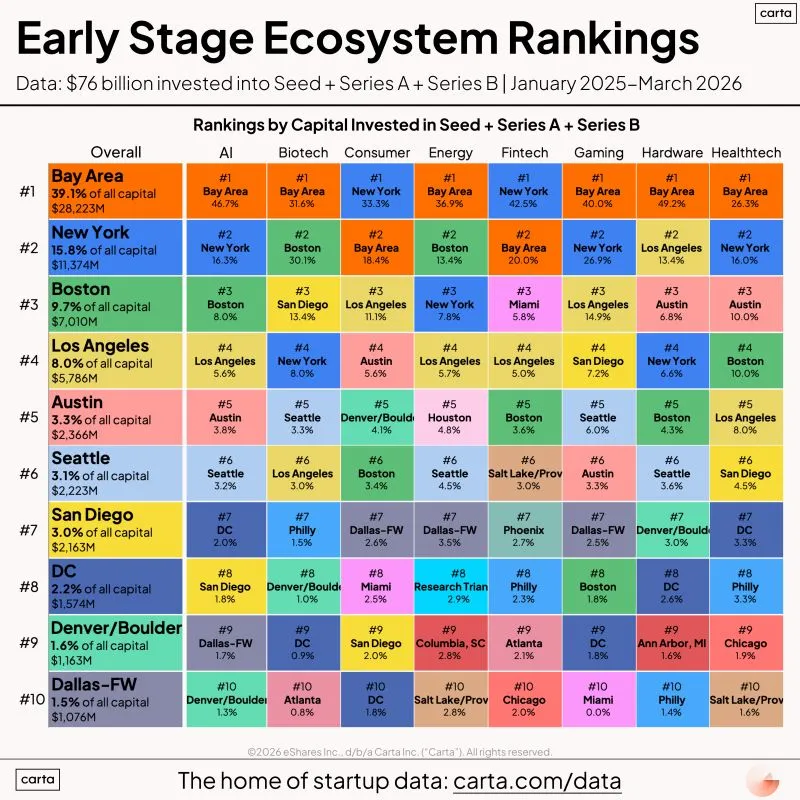

Peter Walker at Carta dropped his latest early-stage ecosystem rankings this week. $76 billion across Seed, Series A, and Series B from January 2025 through March 2026. Dallas-Fort Worth lands at #10 with $1.076 billion, or 1.5% of the total. Ahead of Atlanta, Salt Lake City, Philadelphia, Miami, and Chicago.

A few years ago, Dallas wasn’t on the list at all.

From Lagging to Listed

Peter has been publishing this kind of ecosystem cut for years, and he’s the best public source on this data. His commentary on Dallas, until recently, was consistent and not flattering. In 2023, he singled out DFW and Chicago as the two metros that most underperformed their population base. In late 2024, his trailing twelve-month ranking of Seed and Series A funding had a clean top 10 of Bay Area, NYC, Boston, LA, Seattle, Austin, DC, Denver/Boulder, San Diego, and Chicago. Dallas wasn’t on it. Miami was #11.

Now Dallas is on it.

That’s a real change… an actual movement in the data Carta’s been tracking the whole time. Without Peter’s charts, the trajectory wouldn’t be visible at all.

What Carta Sees (and Doesn’t)

Before getting into what the number says, it’s worth pausing on what the number is.

Carta is cap-table software, not a census. Their data covers the roughly 60,000+ startups using their platform. That’s the largest and most useful dataset of its kind in the public domain, but it’s a sample, not the universe. Some of “Dallas rising” could be Carta penetration rising in Dallas, or Carta penetration declining elsewhere. Without the platform’s market share by metro held constant, the trend line carries some signal noise we can’t fully resolve from the outside.

More importantly, Carta tracks priced venture rounds. Texas private wealth doesn’t move through priced venture rounds the way institutional VC does. Oil and gas fortunes, commercial real estate fortunes, retail fortunes… a lot of Dallas capital flows through family offices and direct investments that never touch a Carta cap table. If Dallas is overweight in venture-adjacent capital that this dataset doesn’t see, the 1.5% number understates the position. That’s plausible. It might also be wishful thinking. The honest answer is the data we have shows 1.5%, and the data we don’t have probably adds to it but we can’t say by how much.

Peter himself broke the ranking into tiers, which is the sharper way to read it. Tier 1 is the Bay Area, alone. Tier 2 is New York, Boston, and LA. Tier 3 is Austin, Seattle, San Diego, DC, and Denver. Tier 4 is Dallas, Miami, Chicago, Salt Lake/Provo, Atlanta, and a long tail behind them.

Dallas is in Tier 4. That’s the honest read, and it’s also the read Peter pairs with an observation worth holding onto… there are now plenty of places across the US where you can raise a solid Seed or Series A round. Ten years ago, that wasn’t true. Tier 4 in 2026 is a meaningfully better place to be a founder than Tier 4 in 2016, which mostly didn’t exist as a tier.

The Lanes That Matter

Here’s the question the top 10 ranking doesn’t answer. Every mature venture ecosystem is anchored by an industrial base it converted into a venture concentration. Boston has biotech because of Harvard, MIT, and a half-century of pharma. New York has fintech because of Wall Street. LA has consumer and hardware because of Hollywood and aerospace. The venture concentration didn’t appear out of nothing. It rode on top of an existing industrial base, and the industrial base did the hard work of training talent, accumulating capital, and seeding spinout opportunities for decades before “venture ecosystem” was even the language used to describe it.

What’s the Dallas-specific lane? The honest answer is there are three plausible ones, in different stages of maturity.

Energy is the obvious one. Texas is the energy capital of the country and has been for a century. The capital, the operators, the supply chains, the regulatory expertise are all here. Dallas shows up at #7 in energy on the Carta chart, which is the best vertical placement the city has. The challenge is that energy venture has historically been hard. Long timelines, heavy capex, political dependencies. The recent push into grid infrastructure, nuclear, and energy transition technologies opens a lane that didn’t exist five years ago. Dallas should own this. The question is whether the local capital base, which knows fossil fuels deeply, can underwrite the energy transition stack with the same conviction.

Healthcare is further along than most people realize. UT Southwestern is a top-tier academic medical center. MassChallenge is running a healthcare-focused cohort in Dallas, which is a national platform allocating real attention to the city. Health Wildcatters has been running a healthcare-specific accelerator here for over a decade and has actual portfolio depth. The Carta chart doesn’t show Dallas in biotech or healthtech, which probably reflects the fact that the institutional infrastructure is real but the breakout rounds haven’t happened yet. That’s a “wait two years and look again” situation, not a “this lane doesn’t exist” situation.

Fintech is the most interesting one, and the one Carta won’t capture for a while.

The financial infrastructure moving into Dallas in the last five years is the kind of thing that historically precedes venture concentration. NYSE Texas launched in January 2026 as a fully electronic exchange headquartered in Dallas. The Texas Stock Exchange, backed by BlackRock and Citadel Securities, is targeting a 2026 launch. Goldman Sachs is building an 800,000 square foot Dallas campus that will house over 5,000 employees by 2028. JPMorgan now employs more people in Texas than in New York. Charles Schwab moved its headquarters here. Bank of America, Wells Fargo, Vanguard have all expanded. The press has started calling it Y’all Street, which is corny enough that it might stick.

This is exactly the kind of pre-venture industrial base that New York leveraged into fintech dominance, except it’s happening in compressed time and in a more business-friendly regulatory environment. None of it shows up on a Carta chart today because Carta tracks startups, not relocations. But if you’re trying to call where fintech founders will be starting companies in 2030, the answer is increasingly some combination of New York, Miami, and Dallas, and the relative weights are shifting.

The lane is real. It just hasn’t shown up in venture data yet because the cycle hasn’t completed. Banks move, then bank talent leaves to start companies, then those companies attract capital, then the capital recycles. Dallas is somewhere in the second step of that loop. Carta will start reflecting it in 2027 and 2028.

The Floor, Not the Ceiling

A few weeks ago I wrote a memo called The Win Condition about four days of events in Dallas that left me thinking the celebration in this ecosystem was outpacing the substance. I stand by it. None of what I said there is contradicted by Dallas being #10 on a Carta chart.

What changes is the floor.

Top 10 is a prerequisite, not an achievement. It’s the price of admission to the conversation that allocators outside Dallas are willing to have. Below the top 10, you’re a regional curiosity. Inside it, you’re someone whose deal flow people will at least open the email about. That distinction matters when you’re trying to syndicate a Series A and the lead is sitting in Menlo Park.

The bar that matters now is whether Dallas can move from 1.5% to 3% over the next five years. Different inputs than getting here did. Getting on the board was a function of population growth, corporate relocations, and a handful of breakout rounds. Moving up the chart requires repeatable institutional infrastructure, deeper local capital, and exits that recycle talent back into the ecosystem. The energy lane needs founders who can underwrite transition technology, not just operators who know the old stack. The healthcare lane needs a few breakout exits to validate the infrastructure that’s already in place. The fintech lane needs the Y’all Street relocation wave to finish converting into founders, which is a 2027-2030 story, not a 2026 one.

So the celebration is real. What’s also real is that #10 with 1.5% means we just got to where the work gets harder. The Bay Area’s lead is structural and won’t close. The competition for Tier 3 is fierce. Standing still gets you back to #11.

Dallas is on the board. That’s the floor. The ceiling is whatever we’re willing to build under it.